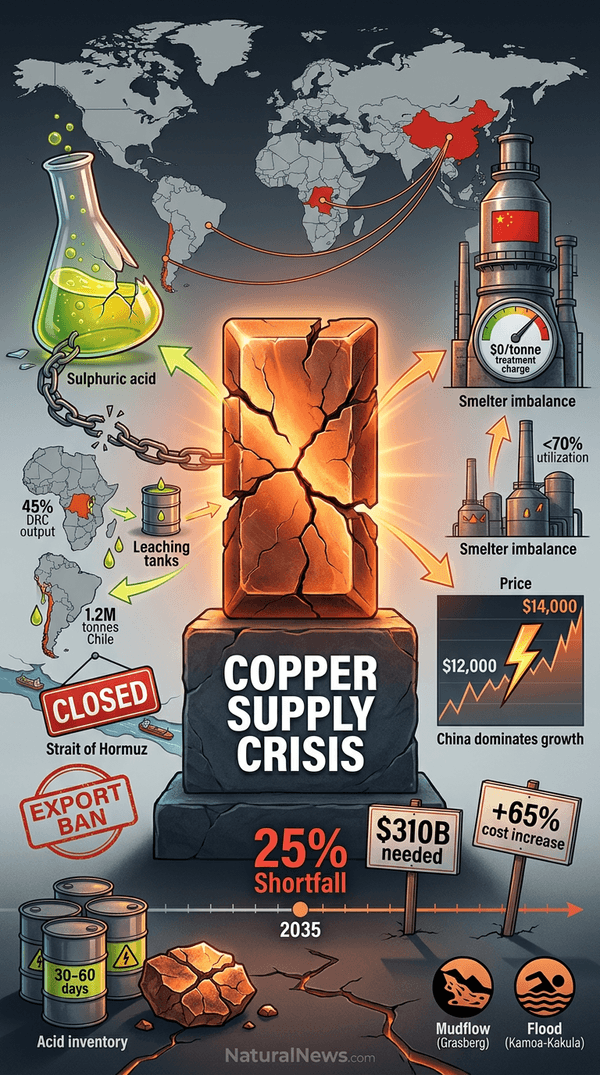

The acid crisis stems from the effective closure of the Strait of Hormuz in February, which choked off roughly half of the global seaborne sulphur trade, combined with a Chinese ban on sulphuric acid exports from May through year-end. The IEA noted that these disruptions endanger leaching-dependent operations in key copper-producing regions, with the Democratic Republic of Congo and Chile most exposed.

Acid crisis threatens key producers

In the Democratic Republic of Congo, nearly 45% of copper production depends on acid leaching, representing about 1.5 million tonnes of output, while Chile relies on leaching for roughly 1.2 million tonnes, according to the IEA. Acid accounts for 20% of costs at DRC solvent extraction and electrowinning facilities, and some producers report acid inventories of only 30 to 60 days, with warnings of potential production curtailments.

The supply chain vulnerabilities exposed by the acid shortage highlight broader concentration risks in the critical minerals sector. As noted in a recent analysis, China dominates the refining and processing of many key metals, a position that leaves other nations dependent on Chinese export policies [1]. The IEA's assessment reinforces concerns that globalized supply chains for essential industrial inputs remain fragile.

Existing disruptions compound supply stress

Disruptions in 2025 wiped out 1.5 million tonnes of mined copper -- over 6% of global supply -- tipping the refined market into deficit, the IEA report states. At Grasberg in Indonesia, production fell to about half of 2024 volumes following a deadly mudflow, with full recovery not expected until 2028. Flooding at the Kamoa-Kakula operation in the DRC cut output nearly a third relative to guidance, according to the agency.

Copper prices have experienced significant volatility in response to supply snags. Earlier in 2025, prices plunged nearly 11% in a single week due to tariff tensions between the United States and China [2]. More recently, the IEA noted that the structural deficit has pushed prices higher, with the metal topping $12,000 a tonne in late 2025 and exceeding $14,000 in May 2026, according to market data cited by the IEA.

Midstream concentration risks grow

The annual treatment charge benchmark for copper concentrates settled at $0 per tonne for 2026, the lowest level ever recorded, and spot fees have remained negative since 2024, the IEA notes. This reflects a severe imbalance between mine supply and smelter capacity, with China accounting for over 90% of global smelter output growth since 2005, lifting its share to half of world supply. Outside China, smelter utilization has fallen below 70%, according to the agency.

Chinese smelters agreed to cut production capacity by over 10% this year, but the IEA stated that reductions are insufficient to balance the market. The agency warned of growing midstream concentration risk similar to that seen in nickel, where a single country's dominance created supply chain vulnerabilities. These risks are compounded by geopolitical tensions; as noted in a recent interview, China's control over copper reserves and processing capacity gives it significant leverage over global supply chains [3].

Long-term supply gap persists despite modest improvement

The IEA projects that primary copper supply will fall about 25% short of requirements in 2035 under current policies, an improvement from last year's 30% gap but still deeply in deficit. Africa accounts for most of the upgrade, with the DRC and Zambia adding nearly 650,000 tonnes to the 2035 outlook, while contributions from Peru, Russia, and Canada also help narrow the gap.

Despite the revision, capital intensity for brownfield expansions has jumped 65% since 2020, lead times for new mines average 17 years, and closing the supply gap requires $310 billion of the $750 billion in mining and refining investment needed through 2040, according to the IEA. These structural constraints mirror broader trends in commodity markets, where chronic underinvestment and rising costs have squeezed supply across a range of metals, as highlighted in earlier analyses of shortages [4].

Demand growth and price outlook

Global refined copper consumption reached nearly 28 million tonnes in 2025, up 3.7%, and is projected to grow over 25% by 2040 driven by grid expansion, electric vehicles, and data centers, according to the IEA's Stated Policies Scenario. Analysts remain split on near-term prices, with forecasts ranging from BMI's average of $12,700 a tonne for 2026 to UBS's $13,000 and Chile's Cochilco at $12,235, according to the report.

The IEA's data signal that the structural story is only beginning, with a market a quarter short of requirements by 2035. As copper becomes increasingly critical for electrification and defense applications, the strain on supply chains may intensify. In a recent interview, Mike Adams highlighted how copper's value extends to unconventional uses, noting that copper-tipped ammunition rounds could become so expensive that users might need to recover and recycle the copper from spent casings [5].

References

- Wattsupwiththat.com. "How China Dominates the World's Critical Minerals Production." April 7, 2026.

- Willow Tohi. "Copper collapse: Tariff war sparks metals meltdown rattles global markets." NaturalNews.com. April 8, 2025.

- Mike Adams. "Mike Adams interview with Andy Schectman." October 31, 2023.

- "Trends-Journal-2021-10-29."

- Mike Adams. "Health Ranger Report - Special Report Americans must prepare for EXTREME POVERTY." Brighteon.com. March 18, 2022.

- NaturalNews.com. "US threatens to leave International Energy Agency over unrealistic green transition push." July 20, 2025.

Explainer Infographic

Please contact us for more information.